Corporate carbon footprint calculations function as the basis for all necessary steps regarding a climate strategy – whether this is a science-based target setting, the identification of effective reduction measures, the compensation of unavoidable residual emissions to achieve climate neutrality or the participation in disclosure programs such as CDP.

However, calculating one´s corporate carbon footprint is often a time-consuming project and limited availability of data can be a hurdle. So-called spend-based carbon accounting uses financial data that is usually already available in companies. In this blog post, we take a closer look at this accounting methodology and explore in which contexts it can be useful.

How does spend-based carbon accounting work?

In spend-based carbon accounting, the economic value of purchased goods or services is multiplied by corresponding emission factors (e.g. kg CO²e per €) to calculate the emissions caused. These calculations are based on so-called environmentally extended input-output (EEIO) models. Spend-based carbon accounting can be time as well as cost saving, as financial data on different purchasing categories is usually available in companies. This enables a carbon footprint calculation with less effort of data collection.

However, this approach comes with limitations. Strong or frequent price fluctuations of the purchased goods, for example, can lead to different results, although the emissions should remain unchanged. Furthermore, exchange rate fluctuations and variating purchasing conditions of different companies complicate the spend-based method, leading to a wide bandwidth of errors. In addition, EEIO data is usually clustered into large product categories only and databases are often limited to specific geographic regions. Thus, the specificity and accuracy we know from using physical-technical emission factors, is not given. How useful is spend-based carbon accounting overall then?

Choosing an appropriate accounting methodology

A robust carbon footprint is particularly important when aiming for climate targets like near- and long-term science-based targets. It is crucial to reflect the progress achieved through implemented reduction measures including those of supply chain partners in the carbon footprints in subsequent years. This progress must not remain invisible due to poor data quality.

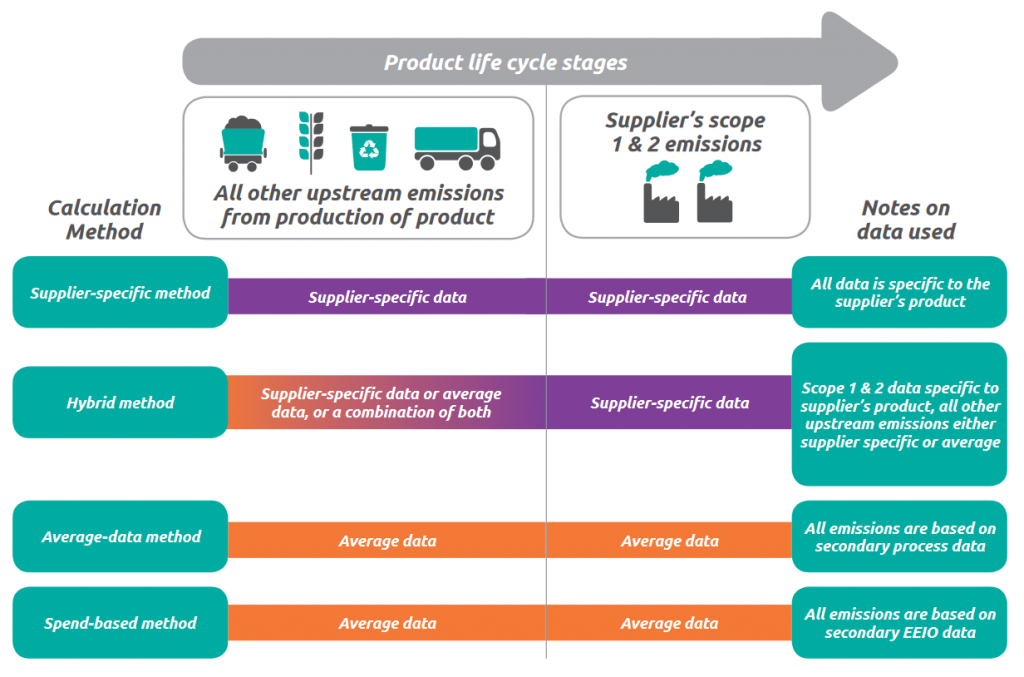

For selecting adequate carbon accounting methodologies, the following principle can be used: Large contributors within a corporate carbon footprint should be calculated with more accurate data and calculation methods, while for small contributors less accurate data and calculation methods may be sufficient to save time and costs.

To identify those large contributors in an initial screening, the spend-based approach is a fast and suitable method. However, physical-technical data offer more specific and accurate results for the further calculation of emissions. Depending on the size of the contributor, average data or even supplier-specific data can be used. The latter provide a better representation of the company’s specific value chain activities and allow companies to better track progress towards the reduction target. At the same time, they are more time and labor intensive and not always available.

In summary, the spend-based method allows a rough approximation of corporate emissions. It can therefore be useful for screening emissions or the calculation of small contributors. Companies that aim for a robust corporate carbon footprint calculation in order to reduce their emissions based on this calculation are advised to use more accurate data and calculation methods. Only a well-conducted corporate carbon footprint provides the suitable basis for further carbon and climate management.

Support through DFGE

At DFGE we are happy to provide you with holistic support in the field of climate strategy. Take now the first step with the calculation of your corporate carbon footprint. Our DFGE TopDown approach makes corporate carbon footprint calculations easier and reduces the time invested. We look forward to supporting you with our more than 20 years of sustainability expertise. Contact us for more information at or +49 8192-99733-20.

Sources

Greenhouse Gas Protocol – Corporate Value Chain Standard

Greenhouse Gas Protocol – Technical Guidance for Calculating Scope 3 Emissions

WWF – Overcoming Barriers for Corporate Scope 3 Action in the Supply Chain