Background and context

Value chain management is the backbone of our interconnected economy, and it has become a key focus of EU regulatory requirements. At the forefront of these regulations is the Corporate Sustainability Due Diligence Directive (CSDDD), which requires companies to identify, prevent, and mitigate human rights and environmental harms across their operations and supply chains. By enforcing accountability, the CSDDD drives significant action throughout businesses.

Complementing these efforts is the Corporate Sustainability Reporting Directive (CSRD), which ensures that companies report on their sustainability practices. One element of the CSRD is ESRS S2, a mandatory reporting standard that requires undertakings to disclose their impacts, risks, and opportunities (IROs), which are connected with the undertakings´ own operations, and their efforts to manage these IROs. In essence, while the CSDDD mandates the due diligence needed to address potential harms, ESRS S2 ensures transparency through standardized disclosures.

Recent debates surrounding the Omnibus Simplification Package have added new layers of uncertainty regarding the scope, timeline, and enforcement of these regulatory requirements. Proposed by the European Commission, the Omnibus Simplification Package aims to reduce the regulatory burden on businesses by amending key sustainability regulations such as the CSDDD, CSRD, CBAM, and the EU Taxonomy. This proposal would delay implementation timelines, narrow reporting scopes, and ease compliance requirements.

Despite these ongoing discussions, the imperative of effective value chain management remains clear. This blog post will outline the current disclosure requirements under ESRS S2 – acknowledging that some data points may be subject to reduction in the near future – and offer practical tips on how to approach compliance with this standard.

The content of ESRS S2

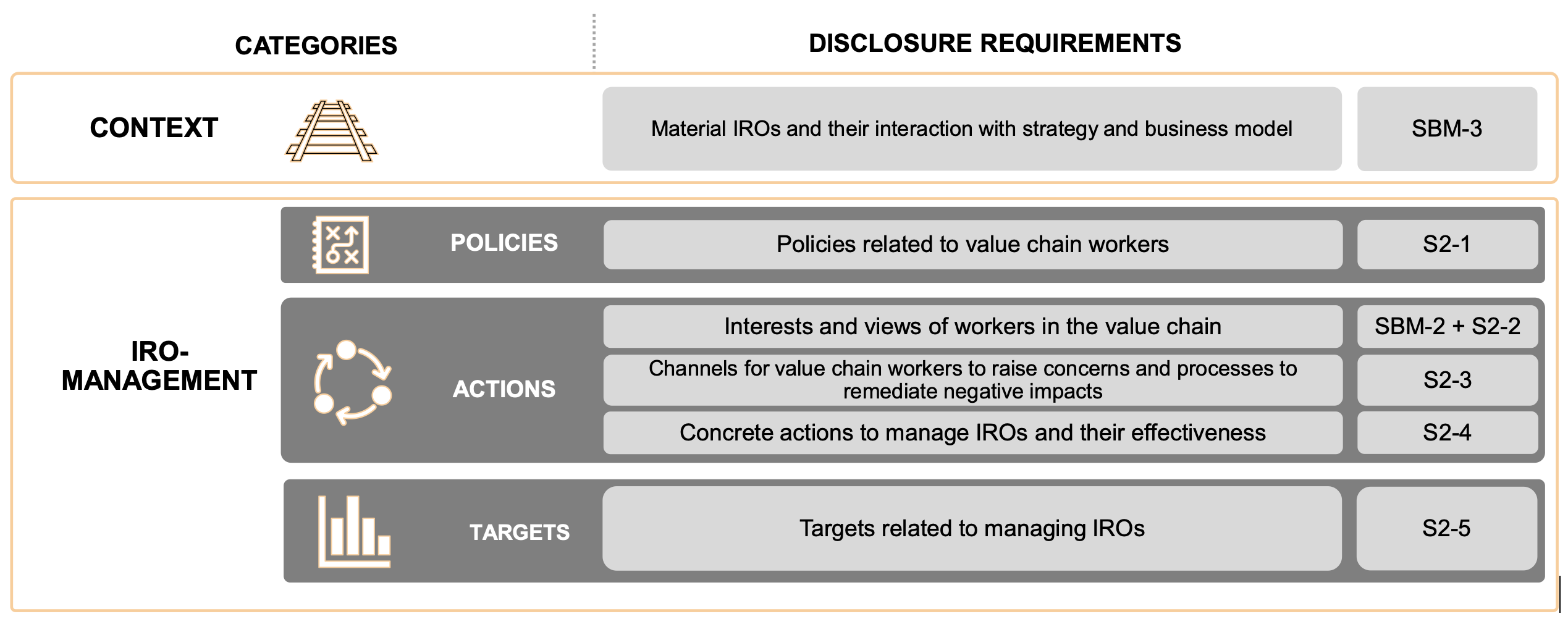

The Standard has seven disclosure requirements, which require information about the IROs and the IRO-management in relaqtion to workers in the value chain.

DISCLOSING THE CONTEXT

- S2 SBM-3: Requires companies to detail their impacts, risks, and opportunities related to their value chain workers, and to explain how these IROs connect with their own operations and business model.

DISCLOSING IRO-MANAGEMENT

- S2-1 – Policies related to value chain workers: Description of policies for managing significant impacts on value chain workers, associated risks and opportunities, human rights commitments, alignment with international standards, and any reported instances of unalignment or non-compliance in the value chain.

- S2-2 & SBM-2 – Processes for engaging with value chain workers about impacts: The undertaking is to describe its engagement with value chain workers (or credible representatives) about the actual and potential impacts on them. It shall indicate whether and how employee perspectives and interests are considered in decision-making, how responsibilities are allocated, whether there are agreements on employee rights, and whether vulnerable employees are included. If such procedures are not in place, this must be disclosed along with a timeframe for implementation.

- S2-3 – Processes to remediate negative impacts and channels for value chain workers to raise concerns: Disclosure requirement on the channels through which value chain workers can speak up and processes for providing remedy to material negative impacts on value chain workers.

- S2-4 – Taking action on managing IROs in relation to value chain workers: Actions and their effectiveness to address significant impacts, risks and opportunities related to value chain workers shall be described. The undertaking shall provide insights into action plans, tracking effectiveness, and respective responses to identified negative impacts as well as methods for mitigation and prevention methods.

- S2-5 – Targets related to managing IROs: Disclosure of time-bound and results-oriented targets set by the company in relation to managing IROs regarding value chain workers. Targets shall relate to the reduction of negative impacts, advancement of positive outcomes, and the management of risks and opportunities for workers. The underlying purpose is to comprehend how targets are used to measure progress and to derive appropriate actions.

Getting started – Tips and advice

To ensure that these disclosure requirements are met efficiently, we recommend the following step-by-step approach:

- Use Synergies with other datahubs: Particularly if you are new to the role of sustainability expert in your company, use existing data to gain a comprehensive overview of available information. Valuable sources include, for example, EcoVadis and IntegrityNext, both of which provide data on value chain workers.

- Start with the context: Begin with disclosure requirement SBM-3 to detail your company’s IROs related to value chain workers and explain how these IROs connect with your own operations and business model. This foundational information supports the fulfillment of subsequent disclosure requirements.

- Think from the end: Use the Theory of Change to structure your approach to the remaining IRO-management disclosure requirements. First, identify your desired goals (S2-5 & S2-1), then work backwards to determine the necessary actions (S2-4) and conditions (S2-2, S2-3) that must be in place. This strategy clarifies the link between activities and goal achievement, leading to better planning and more effective evaluation of your efforts.

Support by the DFGE:

At DFGE, we offer comprehensive support for creating and refining your S2 content. Our services include classical consulting, such as interpreting ESRS requirements and answering specific questions, as well as actively guiding the reporting process—from data collection, validation, and drafting or reviewing CSRD reports to coordinating with auditors. We also provide hands-on assistance in developing policies, measures, and targets, and can take the lead in managing data collection and reporting to ensure you meet S2 requirements effectively and efficiently. We would be happy to support your company in this important topic.

If you have any questions, please contact us via or by phone 08192-99733-20.

Sources: